What is title insurance and should I buy it?

Posted by Tim Bray on

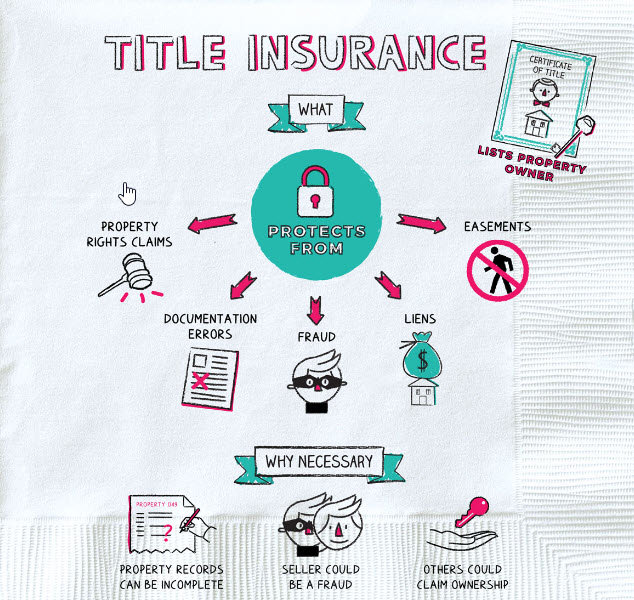

What is title insurance?

Traditional insurance policies protect insureds against future losses. For example, a car insurance policy will protect the driver from future accidents, and a health insurance policy will protect an insured from future health problems. However, title insurance is different because it protects insureds against claims for past occurrences.

Who does title insurance protect?

Two different types of title insurance exist. A real estate owner can choose to purchase title insurance, and lenders can elect to do so. Lenders will require title insurance by mortgagors to secure their security interest in the property. Furthermore, a property owner will purchase title insurance to protect their investment in their property.

…

235 Views, 0 Comments