Unlike the stock market, where most people understand and accept the risk that prices may fall, most people who buy a house don't ever think that the value of their home will ever decrease.

Unlike the stock market, where most people understand and accept the risk that prices may fall, most people who buy a house don't ever think that the value of their home will ever decrease.

The housing market, like other assets, is susceptible to unsustainable gains, and bubbles are formed over time even though many people feel it is a sure bet for growth. That's because of the large transaction costs associated with purchasing a home, not to mention the carrying costs of owning and maintaining a home discourage speculative behavior. However, housing markets do go through periods of irrational exuberance.

This article will help to explain real estate cycles, triggers that cause them, and why consumers should be cognizant of the forces at play before investing in real estate.

What Is a Housing Bubble?

Before we get into the causes of housing bubbles and what makes them pop, it's important to understand a housing bubble itself. They generally begin with a jump in housing demand, despite a limited amount of inventory available. Demand further increases when speculators enter the market, making the bubble bigger. With limited supply and so much demand, prices naturally skyrocket.

Housing bubbles have a direct impact on the real estate industry, but also on homeowners and their personal finances. The impact a bubble can have on the economy—interest rates, lending standards, and practices—can force people to find ways to keep up with their mortgage payments when times get tough. Some may even have to dig deeper into their pockets, using savings and retirement funds just to keep their homes. Housing bubbles are typically a temporary event but have been known to last for years.

Housing Market Bubble Causes

The price of housing, like the price of any good or service in a free market, is driven by supply and demand. When demand increases and/or supply decreases, prices go up. In the absence of a natural disaster that decreases the supply of housing, prices rise because demand trends outpace current supply trends. Just as important is that the supply of housing is slow to react to increases in demand because it takes a long time to build a house, and in highly developed areas there simply isn't any more land to build on. So, if there is a sudden or prolonged increase in demand, prices are sure to rise.

Once you've established that an above-average rise in housing prices is primarily driven by an increase in demand, you may ask what the causes of that increase in demand are. There are several possibilities:

-

An upturn in general economic activity and prosperity puts more disposable income in consumers' pockets and encourages homeownership. (Increase in Incomes) (Stimulus as supplied by the Gov't to prop up the economy)

-

An increase in the population or the demographic segment of the population entering the housing market.

-

A low, general level of interest rates, particularly short-term interest rates, makes homes more affordable.

-

Innovative mortgage products with low initial monthly payments that make homes more affordable.

-

Easy access to credit—a lowering of underwriting standards—that brings more buyers to the market. (Relaxing of Back End Ratios)

-

High-yielding structured mortgage bonds, as demanded by investors, that make more mortgage credit available to borrowers.

-

Potential mispricing of risk by mortgage lenders and mortgage bond investors that expand the availability of credit to borrowers.

-

The short-term relationship between a mortgage broker and a borrower under which borrowers are sometimes encouraged to take excessive risks.

-

A lack of financial literacy and excessive risk-taking by mortgage borrowers.

-

Speculative and risky behavior by home buyers and property investors fueled by unrealistic and unsustainable home price appreciation estimates.

All of these variables can combine to cause a housing market bubble. They tend to feed off of each other. We simply point out that in general, like all bubbles, an uptick in activity and prices precedes excessive risk-taking and speculative behavior by all market participants—buyers, borrowers, lenders, builders, and investors.

Forces that Burst the Bubble

The bubble bursts when excessive risk-taking becomes pervasive throughout the housing system. This happens while the supply of housing is still increasing. In other words, demand decreases while supply increases, resulting in a fall in prices.

This pervasiveness of risk throughout the system is triggered by losses suffered by homeowners, mortgage lenders, mortgage investors, and property investors. Those losses could be triggered by a number of things, including:

-

An increase in interest rates puts homeownership out of reach for some buyers and, in some instances, makes the home a person currently owns unaffordable. This often leads to default and foreclosure, which eventually adds to the current supply available in the market.

-

A downturn in general economic activity leads to less disposable income, job loss, and/or fewer available jobs, which decreases the demand for housing.

-

Demand is exhausted, bringing supply and demand into equilibrium and slowing the rapid pace of home price appreciation that some homeowners, particularly speculators, count on to make their purchases affordable or profitable. When rapid price appreciation stagnates, those who count on it to afford their homes may lose their homes, bringing more supply to the market.

The bottom line is that when losses mount, credit standards are tightened, easy mortgage borrowing is no longer available, demand decreases, supply increases, speculators leave the market, and prices fall.

Housing Market Crash

In the mid-2000s, the U.S. economy experienced a housing bubble that had a direct relationship to the Great Recession. Following the dot-com bubble, values in real estate began to creep up, fueling a rise in homeownership among speculative buyers, investors, and other consumers. Low-interest rates, relaxed lending standards—including low down payment requirements—allowed people who would normally never have been able to purchase a home to become homeowners. This drove home prices up even more.

But many speculative investors stopped buying because the risk was getting too high, leading other buyers to get out of the market. This, in turn, caused prices to drop. Mortgage-backed securities were sold off in massive quantities, while mortgage defaults and foreclosures rose to unprecedented levels.

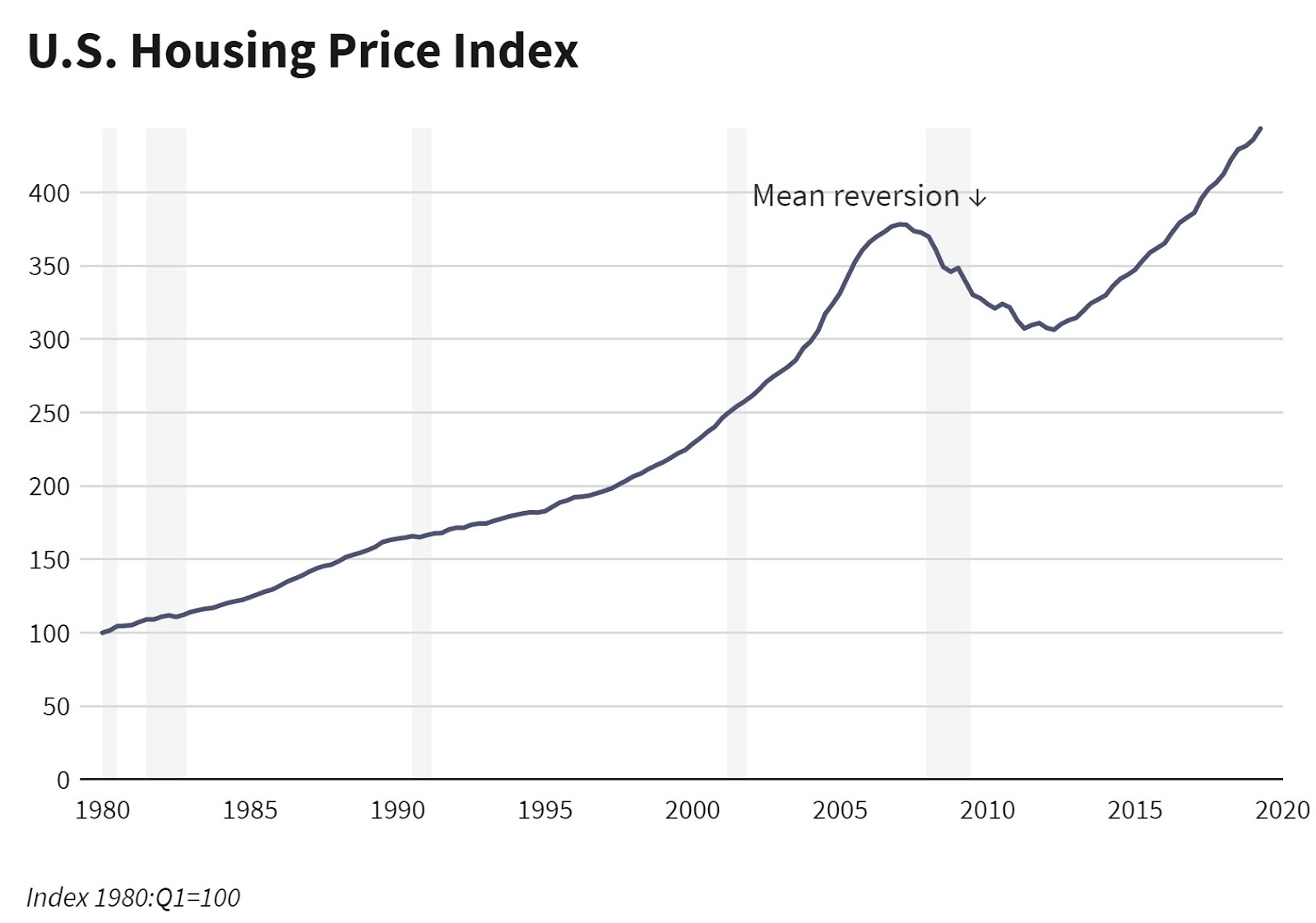

Mean Reversion

Too often, homeowners make the damaging error of assuming recent price performance will continue into the future without first considering the long-term rates of price appreciation and the potential for mean reversion. The laws of physics state that when any object—which has a density greater than air—is propelled upward, it eventually returns to earth because the forces of gravity act upon it. The laws of finance say that markets that go through periods of rapid price appreciation or depreciation will, in time, revert to a price point that puts them in line with where their long-term average rates of appreciation indicate they should be. This is known as mean reversion.

Prices in the housing market follow this law of mean reversion, too. After periods of rapid price appreciation, or, in some cases, depreciation, they revert to where their long-term average rates of appreciation indicate they should be. Home price mean reversion can be either rapid or gradual. Home prices may move quickly to a point that puts them back in line with the long-term average, or they may stay constant until the long-term average catches up with them.

The theoretical value shown above has been derived by calculating the average quarterly percentage increase in the Housing Price Index from the first quarter of 1985 through the fourth quarter of 1998—the approximate point at which home prices began to rise rapidly above the long-term trend. The calculated average quarterly percentage increase was then applied to the starting value shown in the graph and each subsequent value to derive the theoretical Housing Price Index value.

Price Appreciation Estimates

Too many home buyers use recent price performance as benchmarks for what they expect over the next several years. Based on their unrealistic estimates, they take excessive risks. This excessive risk-taking is usually associated with the choice of a mortgage, and the size or cost of the home the consumer purchases. There are several mortgage products that are heavily marketed to consumers and designed to be relatively short-term loans. Borrowers choose these mortgages based on the expectation they will refinance out of that mortgage within a certain number of years and will be able to do so because of the equity they will have in their homes at that point.

Recent home price performance is generally not a good prediction of future home price performance. Homebuyers should look to long-term rates of home price appreciation and consider the financial principle of mean reversion when making important financing decisions. Speculators should do the same.

While taking risks is not inherently bad and, in fact, taking risks is sometimes necessary and advisable, the key to making a good risk-based decision is to understand and measure the risks by making financially sound estimates. This is especially applicable to the largest and most important financial decision most people make—the purchase and financing of a home.

The Bottom Line

Market Cycles exist and can impact your financial well-being as well as the local economy. Working with a true fiduciary who is fact-driven can help you to maximize your returns while minimizing your risks.

How We Can Help

Seaport Real Estate Services offers an array of Advisory Services and proprietary tools that can give you a level of transparency in the marketplace that is very difficult to obtain anywhere else. Our Network of advisors and brokers believe that we can change the local economic landscape by employing sound real estate advice and marketing principles one client at a time.

Written by Barry Neilsen and modified by Tim Bray

Posted by Tim Bray on

Leave A Comment